Though we will try to distinguish between a payment gateway and a payment processor... yet we should crack the key factors that involve a business transaction. Well, let's get to the basics of a business in the first place. It’s you, as a merchant, who provides service or goods to the customer and in response, the customer pays you back. The customer and merchant that we just talked about are the main two players of a transaction procedure. They can also be called the two operators that steer the wheel. However, they don’t physically come to the field to get the services. Instead, they send representatives. The Parties Involved in the Operation

The representatives are their corresponding bank accounts. Now, we have two other parties that bear the same importance during a transaction. Let’s move on using the same setup. In the process, the fund moves from your customer's bank account to your merchant bank account.

To sum it up, the four parties involve in a fund transfer is a customer, the issuing bank, the merchant, and the acquiring bank.

Honesty, you can skip it totally and take it for granted. But as a business proprietor, it’s smart to know all the ends of a transaction. It’ll certainly give you confidence, and in case something gets stuck while receiving your payment, you’ll know where to put the grease.

As you can understand from the intro both the payment gateway and processor have a reciprocal relationship. The job of a payment gateway is to collect and transfer data between the issuing and the acquiring bank. The function of the payment processor is to transfer funds.

The payment processor provides a connection between you and the customer's account. Hence, they can perform a successful transaction. Here, the payment gateway also comes into play. A payment gateway connects your credit card or debit card to the payment processor providing the data.

After that, the processor communicates with both your bank and the customer's bank account. Almost immediately the processor transmits a signal to decline or accept the transaction provided the sufficiency of the customer's bank account.

A payment processor must calculate the purchase cost and adjust it with associate service charges. The payment gateway doesn’t interfere with the merchant or customer account. Whereas the processor possesses more authority to enter into the details of the accounts to add or move funds.

Since there ARE risks involved in fund transfer, the payment processor also takes responsibility to stop fraudulent activities. It checks the security measures to ensures the customer’s data is correct.

The choice of a payment processor solely depends on the merchant. As a business owner, you should know the basics of the payment processor because you have to make the right decision at the end of the day.

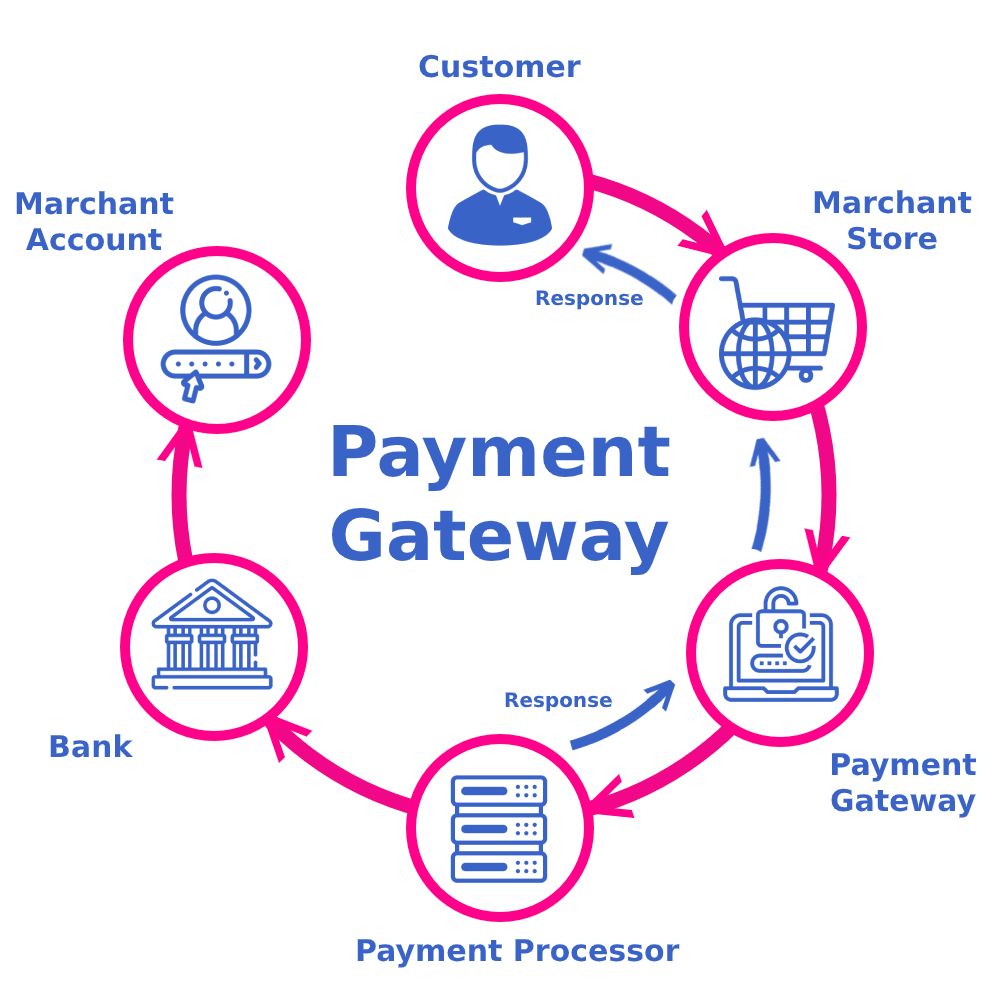

Some people tend to mix up the role of a payment processor with the payment gateway. Put simply, the payment processor works with the information provided by the payment gateway. Here is a step-by-step depiction of a payment processor function.How Does the Payment Processor Work?

After the initial step triggered by the payment gateway, the payment processor transfers the information to the card network. It could be a Visa or MasterCard or anything else preferred by the merchant. The card network checks for the available balance of the cardholder's bank account.

If there is enough balance to make the purchase. The card network returns with the acceptance note to the payment processor. Then it comes back to the payment gateway from where the initial request was sent from.

In the end, the payment processor deposits the fund from the customer's bank account to the merchant bank account, which’s also termed as the acquiring bank account. However, as a merchant, you should know that the funds received by your merchant account need some time to be ready for withdrawal.

Want to go Global? Expand your business in the USA/UK or Business Taxation Help. Feel Free to contact our Specialized Consultant any time.

Book NowBusiness Excellence awards achieved

Businesses guided over five years

Business advices given over 5 years